RH (formerly Restoration Hardware) had a good financial year in the second quarter of 2024, even though the market was tough. The company’s net revenues increased by 3.6% to $830 million, driven by growing demand and strategic initiatives. However, profit margins and overall profitability faced pressure due to higher costs and significant investments into its long-term expansion plans.

Key Insights from RH’s Earning Report:

Below are the key findings from RH’s Q2 earning

- RH reported GAAP operating margins of 11.6% and an adjusted operating margin of 11.7%.

- Adjusted EBITDA margin stood at 17.2%, reflecting solid operational performance.

- The company’s GAAP net income was $29 million, while adjusted net income reached $33 million, both slightly lower than the prior year.

- The company is positioning itself as a global luxury brand with significant expansion plans in North America, Europe, Australia, and the Middle East.

Positive Implications for Investors:

For investors, the positive demand growth and increasing market share are key takeaways. RH’s strategic decisions, including the launch of new RH Interiors Sourcebooks and expansion of luxury product offerings, are yielding results. The company has positioned itself to capture a larger portion of the luxury home furnishings market, particularly as the housing market recovers.

Furthermore, RH’s emphasis on high-end physical retail experiences and hospitality-focused offerings, such as rooftop restaurants and design ateliers, promises to create new revenue streams.

Negative Implications for Investors:

However, challenges remain. RH’s operating and net income margins have shrunk compared to previous periods, due to aggressive investments in its platform expansion during a down market. The company’s cash flow also showed some stress, with negative free cash flow of $37.9 million. Additionally, RH’s stock price may face volatility due to uncertainties in the housing market and its high exposure to interest rate fluctuations. Furthermore, RH’s debt levels remain high, with over $2.4 billion in net debt as of Q2.

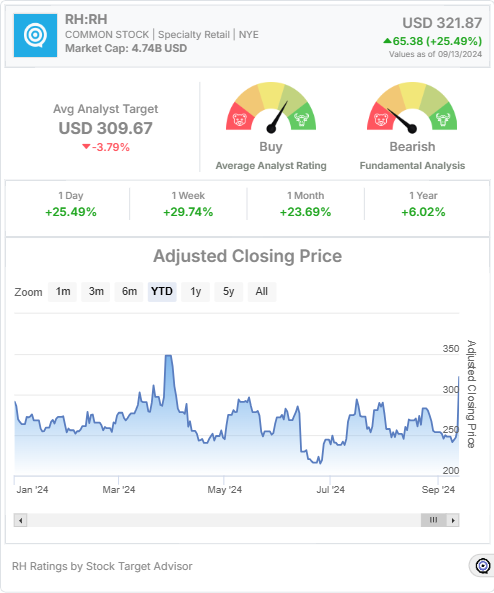

Stock Target Advisor’s Analysis on RH:

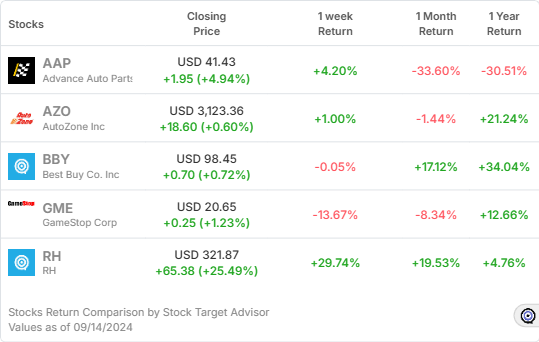

According to Stock Target Advisor’s analysis, RH’s stock shows a bearish outlook, driven by 7 negative signals compared to just 2 positive ones. While RH benefits from positive cash flow and free cash flow, the stock is deemed overvalued in terms of price-to-earnings, price-to-book, and price-to-cash flow ratios. High volatility and lower-than-average capital utilization further add to concerns for cautious investors. The average 12-month target price for RH is $309.67, indicating a slight downside from the current price of $321.87.

Conclusion:

RH’s Q2 2024 results illustrate the company’s resilience in navigating a challenging market, driven by its strategic long-term initiatives. Investors may view RH as a long-term growth play but must remain cautious of its near-term volatility and the overall market environment.

Muzzammil is a content writer at Stock Target Advisor. He has been writing stock news and analysis at Stock Target Advisor since 2023 and has worked in the financial domain in various roles since 2020. He has previously worked on an equity research firm that analyzed companies listed on the stock markets in the U.S. and Canada and performed fundamental and qualitative analyses of management strength, business strategy, and product/services forecast as indicated by major brokers covering the stock.