NVIDIA Corp (NVDA) Earnings

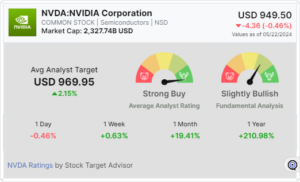

In the latest earnings report, NVIDIA once again showcased impressive performance, surpassing expectations and reinforcing its position as a leader in artificial intelligence (AI) technology. With demand for its products soaring, particularly in the realm of AI, the company has raised its fair value estimate to $1,050 from $910. Let’s delve into the details of NVIDIA’s earnings and explore the factors driving its growth.

Business Description

NVIDIA is renowned for its graphics processing units (GPUs), which were initially developed for enhancing gaming experiences but have since found extensive applications in AI. Alongside AI GPUs, the company offers the CUDA software platform, essential for AI model development and training. Additionally, NVIDIA is expanding its presence in data center networking solutions, facilitating the handling of complex workloads.

Business Strategy & Outlook

NVIDIA’s wide economic moat stems from its market leadership in GPUs and the establishment of high customer switching costs around its proprietary software, notably the CUDA platform. The company’s GPUs excel in parallel processing, a crucial capability for accelerating AI workloads, positioning NVIDIA as a dominant player in AI model training.

Bulls Say

- NVIDIA’s GPUs boast industry-leading parallel processing capabilities, essential for diverse applications like gaming, AI, and cryptocurrency mining.

- The company’s dominance in data center GPUs and the CUDA software platform solidifies its position in AI model training, poised for exponential growth.

- NVIDIA’s early mover advantage in autonomous driving technology presents significant opportunities for widespread adoption.

Bears Say

- While NVIDIA leads in AI chip technology, competitors and tech giants are investing in in-house chip development, potentially posing future challenges.

- Greater competition in AI training software may emerge, challenging NVIDIA’s stronghold with the CUDA platform.

- Fluctuations in demand for gaming GPUs, historically subject to boom-or-bust cycles, pose risks to NVIDIA’s revenue stability.

Economic Moat

Morningstar assigns NVIDIA a wide economic moat rating, attributing it to intangible assets surrounding its GPUs and the significant switching costs associated with the CUDA platform.

Fair Value and Profit Drivers

Revenue for the April quarter reached $26.0 billion, surpassing expectations and reflecting robust growth, particularly in data center revenue, which accounted for 87% of total revenue. The company’s adjusted gross margin expanded sequentially to 78.9%, underscoring its exceptional pricing power.

Risk and Uncertainty

Despite NVIDIA’s strong performance, risks remain, including potential competition from in-house chip solutions developed by tech giants and fluctuations in demand for gaming GPUs.

Capital Allocation

NVIDIA’s exemplary capital allocation strategy underscores its commitment to long-term growth and shareholder value creation.

In conclusion, NVIDIA’s latest earnings report reaffirms its position as a frontrunner in AI technology, with demand for its products continuing to surge. While risks persist, the company’s strategic initiatives and market leadership bode well for sustained growth in the foreseeable future.

STA Research (StockTargetAdvisor.com) is a independent Investment Research company that specializes in stock forecasting and analysis with integrated AI, based on our platform stocktargetadvisor.com, EST 2007.