Global Markets

Canadian Markets

Canadian stocks edged modestly higher as improving domestic macro data helped stabilize sentiment heading into the second quarter. Statistics Canada reported that real GDP expanded by 0.5% in April, marking the strongest monthly gain since mid-2025 and signalling that the Canadian economy had re-entered expansion after entering a recession.

Gains were led primarily by basic materials and financials, two sectors that are highly sensitive to macroeconomic expectations and commodity cycles. Materials benefited from ongoing positioning in precious metals and industrial metals despite a broader softening in commodity prices. Financials also advanced, supported by improving growth expectations and increased investor focus on structural productivity gains, particularly the potential for AI-driven efficiency and credit analytics improvements in banking and insurance operations.

American Markets

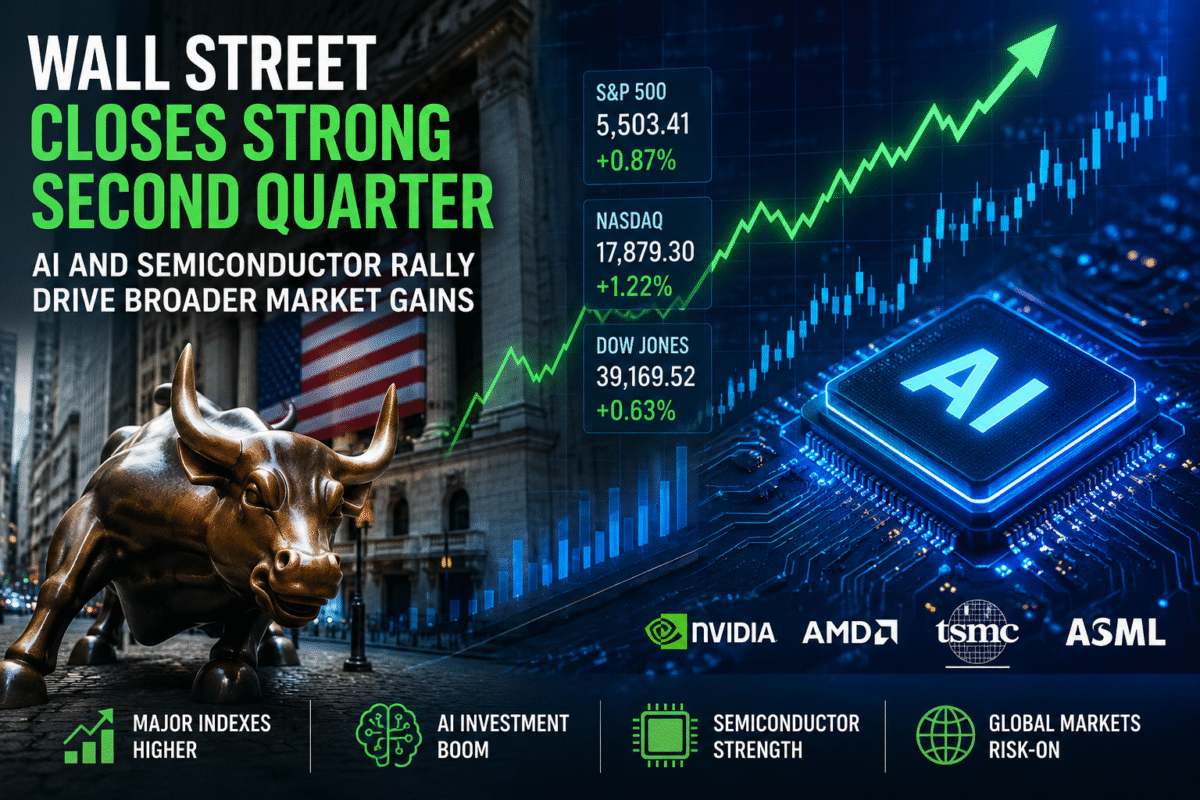

U.S. stocksrose broadly as Wall Street wrapped up a strong second quarter, with investor optimism remaining firmly centered on the semiconductor sector and the ongoing artificial intelligence investment boom. Chipmakers and AI-related technology companies continued to attract significant capital flows as investors bet that accelerating demand for advanced processors, cloud infrastructure, and data-center capacity will drive robust earnings growth over the coming years. The rally was fueled by expectations that businesses across industries will increase spending on AI technologies, benefiting companies involved in semiconductor design, manufacturing equipment, networking hardware, and software platforms.

The technology-led advance helped push major indexes higher and reinforced a broader risk-on sentiment across financial markets. Investors largely looked past concerns surrounding interest rates and global economic growth, focusing instead on strong corporate earnings prospects and expanding AI adoption.

The strength in technology stocks also supported gains across other sectors as improving market confidence encouraged investors to increase exposure to equities. Financials, industrials, and consumer discretionary shares benefited from the positive market tone, while declining volatility signaled growing confidence in the economic outlook. As a result, U.S. markets ended the quarter on a strong footing, with the AI-driven technology rally remaining the primary catalyst behind equity market performance and investor enthusiasm heading into the second half of the year.

European Markets

European markets also moved higher, with stocks setting the strongest quarterly performance in over five years, supported by improving growth expectations and sustained optimism around artificial intelligence investment cycles.

In the United Kingdom, stocks gained, underpinned by strength in defence and financial stocks, and extended its streak of six quarterly gains, reflecting resilient corporate earnings and a more stable macro backdrop. UK growth for Q1 2026 was confirmed at 0.6%, while late-2025 GDP was revised slightly downward to 0.1%, indicating that while the economy continues to expand, the pace remains uneven and sensitive to external shocks, like inflationary pressures.

Corporate Stock News

AbbVie Inc (ABBV) & Merck & Co Inc (MRK): U.S. lawmakers have launched a national security review into whether clinical trials conducted in China may have supported Chinese military capabilities, requesting detailed disclosures on due diligence, data protection, and trial standards, particularly in Xinjiang and military-linked hospitals.

Alphabet Inc (GOOGL) & Apple Inc (AAPL): The UK Competition and Markets Authority proposed easing restrictions on app developers by allowing them to direct users to external payment options outside Apple’s App Store and Alphabet’s Google Play, aiming to reduce fees and increase competition, with any platform “steering” fees required to be fair and lower than current commissions.

Amazon.com Inc (AMZN): Australia’s competition regulator has taken Amazon’s Australian unit to court over allegations that Prime Video subscription terms unfairly allowed the introduction of advertising without compensation to users, affecting over one million subscribers.

Amgen Inc (AMGN): The New England Journal of Medicine retracted a key clinical trial study supporting Amgen’s rare-disease drug after regulatory findings indicated altered patient data and instances of researchers being unblinded during the trial process.

Astrana Health Inc (ASTH): Jefferies raised its price target to $53 from $43, citing stable Medicaid-related commentary consistent with prior guidance.

Berkshire Hathaway Inc (BRK.A) (BRK.B): Warren Buffett is delaying his mid-year donation to the Gates Foundation pending a review into the foundation’s historical ties to Jeffrey Epstein, with a decision potentially pushed to his annual Thanksgiving letter period.

Blackstone Inc (BX) & Digital Realty Trust Inc (DLR): Digital Realty Trust is acquiring Blackstone’s 80% stake in two Virginia data centers and a 50% stake in a third in a $3.5 billion cash-and-stock transaction, expanding its data center footprint while Blackstone monetizes its holdings.

Cal-Maine Foods Inc (CALM): The U.S. Department of Justice and 17 states settled with major egg producers, including Cal-Maine, over alleged price manipulation, with financial penalties and large egg donations to food banks.

Concentrix Corp (CNXC): The company cut its full-year revenue and profit outlook due to weaker client spending amid financial pressure, triggering a sharp share decline after earnings.

Dominion Energy Inc (D) & NextEra Energy Inc (NEE): Senator Angus King urged regulators to reject NextEra’s $66.8 billion acquisition of Dominion Energy, arguing it would concentrate excessive market power and reduce competition in regional energy markets.

Eli Lilly and Co (LLY): Eli Lilly transferred China commercialization rights for its breast cancer drug Verzenios to Innovent Biologics amid intensifying generic competition in the Chinese market.

Empery Digital Inc (EMPD): Empery Digital is partnering with major real estate and energy-linked investors to repurpose a Midwest facility into a data center and pursue a potential $1 billion hyperscaler leasing agreement.

Ford Motor Co (F): Ford is recalling over 740,000 U.S. vehicles due to a transmission defect that could affect park functionality and increase rollaway risk, alongside a separate recall of Bronco vehicles for improperly secured fender flares.

Honeywell International Inc (HON): Daiwa Capital Markets raised its price target to $255 from $240, citing expectations for steady earnings growth from 2026 through 2028.

Ralph Lauren Corp (RL): Ralph Lauren’s China growth is being driven by long-term brand repositioning and a shift in Chinese consumer preferences toward mid-to-upper luxury value brands rather than short-term cyclical demand.

Regeneron Pharmaceuticals Inc (REGN): The FDA selected Regeneron among several companies for a pilot program to speed up reviews of new domestic drug manufacturing facilities as part of efforts to strengthen U.S. pharmaceutical supply chains.

Uber Technologies Inc (UBER): Uber and Waymo ended their autonomous vehicle partnership in Phoenix, with Uber shifting toward a new autonomous strategy while Waymo continues operating its fleet independently and maintains limited availability on Uber in other cities.

Walt Disney Co (DIS): JPMorgan raised Disney’s price target to $140 from $139, citing improved outlook guidance and anticipated support from upcoming film releases including major franchise titles.

STA Research (StockTargetAdvisor.com) is a independent Investment Research company that specializes in stock forecasting and analysis with integrated AI, based on our platform stocktargetadvisor.com, EST 2007.