Chubb Ltd (CB) reported its earnings for the second quarter 2024 yesterday, highlighting significant financial growth and resilience despite challenging market conditions. This report delves into Chubb’s financial performance, examining the key aspects impacting its stock price and investor sentiment.

Key Insights from Chubb’s Q2 Reports:

Chubb reported a substantial increase in its financial metrics for the second quarter of 2024. Net income per share surged by 26.4% to $5.46, while core operating income per share rose by 9.3% to $5.38. The consolidated net premiums written grew by 11.8%, reaching $13.4 billion, with property and casualty (P&C) premiums up by 10.6% and life insurance premiums up by 27.6%. The P&C combined ratio improved to 86.8%, indicating efficient underwriting practices.

Net income for the quarter was $2.23 billion, a 24.3% increase, while core operating income stood at $2.20 billion, up 7.5%. For the first half of 2024, net income totaled $4.37 billion, up 18.7%, and core operating income was a record $4.41 billion, up 13.5%. These figures underscore Chubb’s robust financial health and strategic growth initiatives.

Positive Implications for Investors:

Investors can find several positive takeaways from Chubb’s Q2 performance:

- Strong Financial Growth: The significant increases in net income and core operating income reflect Chubb’s effective management and growth strategies.

- Premium Growth: The 11.8% rise in consolidated net premiums written, especially the 27.6% increase in life insurance premiums, indicates robust demand and market expansion.

- Efficient Underwriting The P&C combined ratio of 86.8% and the record low combined ratio of 83.2% excluding catastrophe losses demonstrate Chubb’s underwriting proficiency.

- Investment Income: Pre-tax net investment income soared by 28.2% to $1.47 billion, marking a record high. This boost in investment income contributes significantly to overall profitability.

Negative Implications for Investors:

Despite the positive performance, there are a few areas of concern for investors:

- Catastrophe Losses: Pre-tax catastrophe losses increased to $580 million compared to $400 million last year, indicating higher exposure to catastrophic events.

- Foreign Exchange Losses The book value per share was negatively impacted by $457 million in foreign exchange losses, reflecting vulnerabilities in international operations.

- High Valuation Metrics Chubb’s stock is trading at high multiples relative to its book and cash flow values, which may deter value-focused investors.

Stock Target Advisor’s Analysis on Chubb:

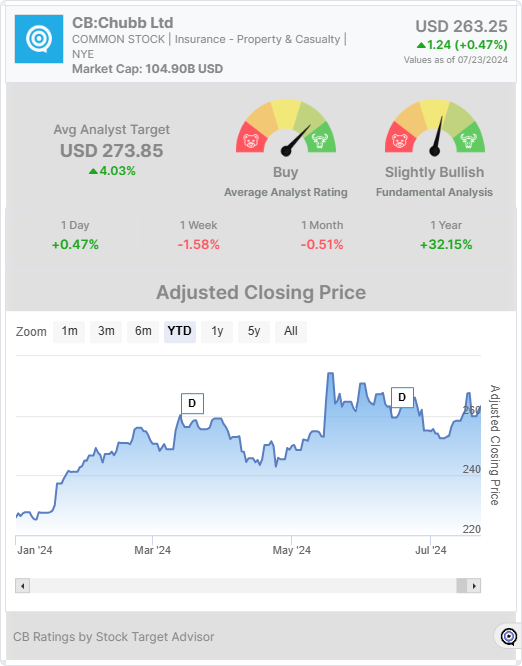

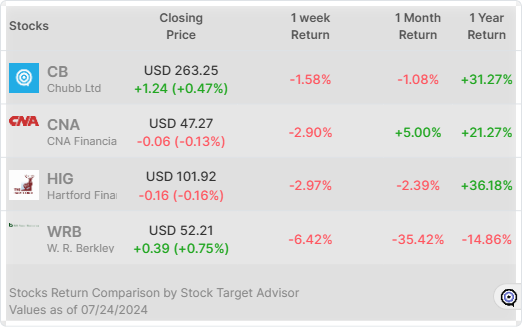

Stock Target Advisor provides a slightly bullish outlook on Chubb Ltd, supported by four positive signals against three negative ones. Analysts have set an average target price of USD 273.85 over the next 12 months, with a predominant “Buy” rating. The stock has experienced a 1.60% increase over the past week and a 31.27% rise over the past year, reflecting strong market confidence. However, it is noted that Chubb’s stock is considered overpriced compared to its peers on book value and cash flow bases, advising cautious investment.

Conclusion:

Chubb’s second-quarter earnings report presents a compelling case for its strong financial health and growth potential. Investors are advised to consider both the growth prospects and valuation concerns when making investment decisions regarding Chubb Ltd.

Muzzammil is a content writer at Stock Target Advisor. He has been writing stock news and analysis at Stock Target Advisor since 2023 and has worked in the financial domain in various roles since 2020. He has previously worked on an equity research firm that analyzed companies listed on the stock markets in the U.S. and Canada and performed fundamental and qualitative analyses of management strength, business strategy, and product/services forecast as indicated by major brokers covering the stock.